Which are the correct steps, in order, to deal with the loss of an online redo log if the database has not yet crashed?() a. Issue a checkpoint. b. Shut down the database. c. Issue an alter database open command to open the database. d. Startup mount the database. e. Issue an alter database clear logfile command. f. Recover all database datafiles.

第1题:

Which of the following would be the best title for the passage?

A. Saving Energy Starts at Home

B. Changing Our Habits Begins at Work

C. Changing Climate Sounds Reasonable

D. Reading Emissions of Proves CO2 Difficult

第2题:

1 Your client, Island Co, is a manufacturer of machinery used in the coal extraction industry. You are currently planning

the audit of the financial statements for the year ended 30 November 2007. The draft financial statements show

revenue of $125 million (2006 – $103 million), profit before tax of $5·6 million (2006 – $5·1 million) and total

assets of $95 million (2006 – $90 million). Your firm was appointed as auditor to Island Co for the first time in June

2007.

Island Co designs, constructs and installs machinery for five key customers. Payment is due in three instalments: 50%

is due when the order is confirmed (stage one), 25% on delivery of the machinery (stage two), and 25% on successful

installation in the customer’s coal mine (stage three). Generally it takes six months from the order being finalised until

the final installation.

At 30 November, there is an amount outstanding of $2·85 million from Jacks Mine Co. The amount is a disputed

stage three payment. Jacks Mine Co is refusing to pay until the machinery, which was installed in August 2007, is

running at 100% efficiency.

One customer, Sawyer Co, communicated in November 2007, via its lawyers with Island Co, claiming damages for

injuries suffered by a drilling machine operator whose arm was severely injured when a machine malfunctioned. Kate

Shannon, the chief executive officer of Island Co, has told you that the claim is being ignored as it is generally known

that Sawyer Co has a poor health and safety record, and thus the accident was their fault. Two orders which were

placed by Sawyer Co in October 2007 have been cancelled.

Work in progress is valued at $8·5 million at 30 November 2007. A physical inventory count was held on

17 November 2007. The chief engineer estimated the stage of completion of each machine at that date. One of the

major components included in the coal extracting machinery is now being sourced from overseas. The new supplier,

Locke Co, is located in Spain and invoices Island Co in euros. There is a trade payable of $1·5 million owing to Locke

Co recorded within current liabilities.

All machines are supplied carrying a one year warranty. A warranty provision is recognised on the balance sheet at

$2·5 million (2006 – $2·4 million). Kate Shannon estimates the cost of repairing defective machinery reported by

customers, and this estimate forms the basis of the provision.

Kate Shannon owns 60% of the shares in Island Co. She also owns 55% of Pacific Co, which leases a head office to

Island Co. Kate is considering selling some of her shares in Island Co in late January 2008, and would like the audit

to be finished by that time.

Required:

(a) Using the information provided, identify and explain the principal audit risks, and any other matters to be

considered when planning the final audit for Island Co for the year ended 30 November 2007.

Note: your answer should be presented in the format of briefing notes to be used at a planning meeting.

Requirement (a) includes 2 professional marks. (13 marks)

第3题:

The Japanese Quality Control (QC) Circle movement motivated its participants in many ways. Which of the following represents the most important motivation for the QC circle participants?

A . improving the performance of the company

B . self-improvement

C . financial incentives

D . recognition among co-workers

E . strengthening of relationships between co-workers

第4题:

One of the disadvantages of using carbon dioxide to extinguish a fire in an enclosed space is

A.the 'snow' which is sometimes discharged along with the gas is toxic

B.prolonged exposure to high concentrations of CO2 gas causes suffocation

C.rapid dissipation of the CO2 vapor

D.the CO2 gas is lighter than air and a large amount is required to extinguish a fire near the deck

第5题:

4 You are a senior manager in Becker & Co, a firm of Chartered Certified Accountants offering audit and assurance

services mainly to large, privately owned companies. The firm has suffered from increased competition, due to two

new firms of accountants setting up in the same town. Several audit clients have moved to the new firms, leading to

loss of revenue, and an over staffed audit department. Bob McEnroe, one of the partners of Becker & Co, has asked

you to consider how the firm could react to this situation. Several possibilities have been raised for your consideration:

1. Murray Co, a manufacturer of electronic equipment, is one of Becker & Co’s audit clients. You are aware that the

company has recently designed a new product, which market research indicates is likely to be very successful.

The development of the product has been a huge drain on cash resources. The managing director of Murray Co

has written to the audit engagement partner to see if Becker & Co would be interested in making an investment

in the new product. It has been suggested that Becker & Co could provide finance for the completion of the

development and the marketing of the product. The finance would be in the form. of convertible debentures.

Alternatively, a joint venture company in which control is shared between Murray Co and Becker & Co could be

established to manufacture, market and distribute the new product.

2. Becker & Co is considering expanding the provision of non-audit services. Ingrid Sharapova, a senior manager in

Becker & Co, has suggested that the firm could offer a recruitment advisory service to clients, specialising in the

recruitment of finance professionals. Becker & Co would charge a fee for this service based on the salary of the

employee recruited. Ingrid Sharapova worked as a recruitment consultant for a year before deciding to train as

an accountant.

3. Several audit clients are experiencing staff shortages, and it has been suggested that temporary staff assignments

could be offered. It is envisaged that a number of audit managers or seniors could be seconded to clients for

periods not exceeding six months, after which time they would return to Becker & Co.

Required:

Identify and explain the ethical and practice management implications in respect of:

(a) A business arrangement with Murray Co. (7 marks)

第6题:

JOL Co was the market leader with a share of 30% three years ago. The managing director of JOL Co stated at a

recent meeting of the board of directors that: ‘our loss of market share during the last three years might lead to the

end of JOL Co as an organisation and therefore we must address this issue immediately’.

Required:

(b) Discuss the statement of the managing director of JOL Co and discuss six performance indicators, other than

decreasing market share, which might indicate that JOL Co might fail as a corporate entity. (10 marks)

第7题:

4 You are an audit manager in Nate & Co, a firm of Chartered Certified Accountants. You are reviewing three situations,

which were recently discussed at the monthly audit managers’ meeting:

(1) Nate & Co has recently been approached by a potential new audit client, Fisher Co. Your firm is keen to take the

appointment and is currently carrying out client acceptance procedures. Fisher Co was recently incorporated by

Marcellus Fisher, with its main trade being the retailing of wooden storage boxes.

(2) Nate & Co provides the audit service to CF Co, a national financial services organisation. Due to a number of

errors in the recording of cash deposits from new customers that have been discovered by CF Co’s internal audit

team, the directors of CF Co have requested that your firm carry out a review of the financial information

technology systems. It has come to your attention that while working on the audit planning of CF Co, Jin Sayed,

one of the juniors on the audit team, who is a recent information technology graduate, spent three hours

providing advice to the internal audit team about how to improve the system. As far as you know, this advice has

not been used by the internal audit team.

(3) LA Shots Co is a manufacturer of bottled drinks, and has been an audit client of Nate & Co for five years. Two

audit juniors attended the annual inventory count last Monday. They reported that Brenda Mangle, the new

production manager of LA Shots Co, wanted the inventory count and audit procedures performed as quickly as

possible. As an incentive she offered the two juniors ten free bottles of ‘Super Juice’ from the end of the

production line. Brenda also invited them to join the LA Shots Co office party, which commenced at the end of

the inventory count. The inventory count and audit procedures were completed within two hours (the previous

year’s procedures lasted a full day), and the juniors then spent four hours at the office party.

Required:

(a) Define ‘money laundering’ and state the procedures specific to money laundering that should be considered

before, and on the acceptance of, the audit appointment of Fisher Co. (5 marks)

第8题:

165 The Japanese Quality Control (QC) Circle movement motivated its participants in many ways. Which of the following represents the most important motivation for the QC circle participants?

A. improving the performance of the company

B. self-improvement

C. financial incentives

D. recognition among co-workers

E. strengthening of relationships between co-workers

第9题:

You need to describe the various types of flow control to your co-workers. Which of the following are types of flow control that can be used in a network? (Choose three)

A. Congestion avoidance

B. Windowing

C. Cut-through

D. Buffering

E. Load Balacing

F. Fast Forward

第10题:

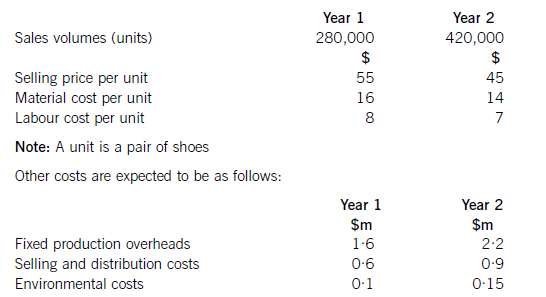

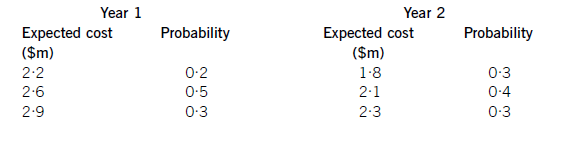

Shoe Co, a shoe manufacturer, has developed a new product called the ‘Smart Shoe’ for children, which has a built-in tracking device. The shoes are expected to have a life cycle of two years, at which point Shoe Co hopes to introduce a new type of Smart Shoe with even more advanced technology. Shoe Co plans to use life cycle costing to work out the total production cost of the Smart Shoe and the total estimated profit for the two-year period.

Shoe Co has spent $5·6m developing the Smart Shoe. The time spent on this development meant that the company missed out on the opportunity of earning an estimated $800,000 contribution from the sale of another product.

The company has applied for and been granted a ten-year patent for the technology, although it must be renewed each year at a cost of $200,000. The costs of the patent application were $500,000, which included $20,000 for the salary costs of Shoe Co’s lawyer, who is a permanent employee of the company and was responsible for preparing the application.

The following information is also available for the next two years:

Shoe Co is still negotiating with marketing companies with regard to its advertising campaign, so is uncertain as to what the total marketing costs will be each year. However, the following information is available as regards the probabilities of the range of costs which are likely to be incurred:

Required:

Applying the principles of life cycle costing, calculate the total expected profit for Shoe Co for the two-year period.

(10 marks)